[ad_1]

Average credit card rates top 20%

Most credit cards come with a variable rate, which has a direct connection to the Fed’s benchmark rate.

After a prolonged period of rate hikes, the average credit card rate is now more than 20% on average — an all-time high, while balances are higher and nearly half of credit card holders carry credit card debt from month to month, according to a Bankrate report.

“Yet another rate hike from the Fed means today’s sky-high credit card interest rates will rise even further in the very near future,” said Matt Schulz, chief credit analyst at LendingTree. Cardholders should expect their current cards’ interest rates to rise in the next billing cycle or two, he said.

Mortgage rates now average around 6.5%

Peopleimages | Istock | Getty Images

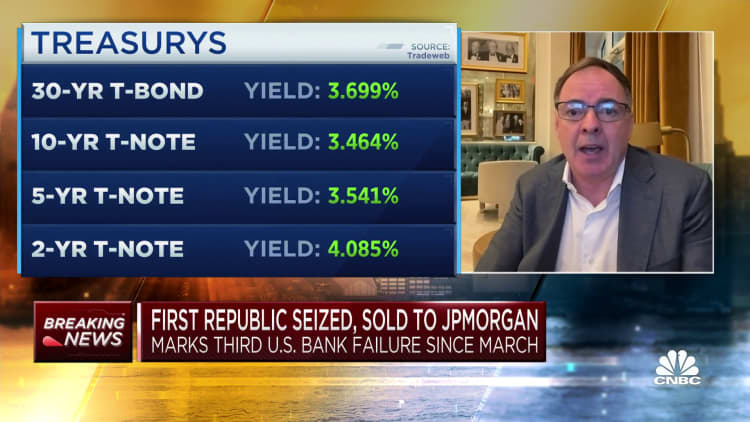

Although 15-year and 30-year mortgage rates are fixed, and tied to Treasury yields and the economy, anyone shopping for a new home has lost considerable purchasing power, partly because of inflation and the Fed’s policy moves.

The average rate for a 30-year, fixed-rate mortgage currently sits at 6.48%, according to Bankrate, down slightly from November’s high but still much higher than it was a year ago.

“While borrowers can save money relative to what they would have paid for a mortgage a few months ago, they’re still going to be shelling out much more than they would have had they bought a home at the start of last year,” said Jacob Channel, senior economic analyst at LendingTree.

“All in all, there’s no getting around just how tough today’s housing market is for many people to break into and navigate.”

They’re still going to be shelling out much more than they would have had they bought a home at the start of last year.

Jacob Channel

senior economic analyst at LendingTree

Auto loan rates rose to more than 6.5%

The average rate on a five-year new car loan is now 6.58%, according to Bankrate.

Keeping up with the higher cost has become a challenge, research shows, with more borrowers falling behind on their monthly loan payments.

Federal student loans are already near 5%

Wavebreakmedia | Istock | Getty Images

For now, anyone with existing federal education debt will benefit from rates at 0% until the payment pause ends, which the U.S. Department of Education expects to happen sometime this year.

Private student loans tend to have a variable rate tied to the Libor, prime or Treasury bill rates — and that means that, as the Fed raises rates, those borrowers will also pay more in interest. How much more, however, will vary with the benchmark.

Deposit rates at some banks are up to 4.5%

While the Fed has no direct influence on deposit rates, the yields tend to be correlated to changes in the target federal funds rate. The savings account rates at some of the largest retail banks, which were near rock bottom during most of the Covid pandemic, are currently up to 0.39%, on average.

Thanks, in part, to lower overhead expenses, top-yielding online savings account rates are as high as 4.5%, according to Bankrate.

However, if this is the Fed’s last increase for a while, then deposit rate hikes are likely to slow, according to Ken Tumin, founder of DepositAccounts.com.

But “it’s not too late,” said Greg McBride, chief financial analyst at Bankrate.com. “We may not see much more in the way of improvement but there’s still a substantial advantage,” he said of switching to a high-yield savings account.

“There’s no advantage to staying where you are if you haven’t benefited from rising rates.”

[ad_2]

{kind=link}